How the road freight transport market works in Russia

The cheapest way to deliver raw materials or finished goods from the manufacturer to the consumer is considered to be the railway - but due to the fact that its network is unevenly distributed throughout Russia, and Russian Railways is a huge bureaucratic machine, when talking about freight transportation, we are most often talking about road transport. It would seem that in Russia they produce ordinary trucks and truck tractors (not only KAMAZ, but also, for example, Volvo), roads are gradually being repaired while there is still cargo - this market should be attractive.

In practice, however, this does not happen. Unlike the same railway, there are no traces of a monopoly in road freight transportation - according to some data, the 10 largest transport companies in Russia account for less than 16% of freight turnover

. The basis of the market is small private carriers, often even individual entrepreneurs (who can be both the owner and the driver at the same time).

It is not so easy to attribute this to problems in the economy - according to official data, until 2020, industrial production grew, as did retail trade. This means that there are loads

– but why then do carriers complain so much about the lack of income?

Most participants in the road transportation market believe that the market now belongs entirely to customers. In simple terms, this means that the customer can choose from a variety of carriers - most likely the one who offers the lowest price. And this happened, as the industry believes, due to the active development of electronic services for booking transportation.

Some people call this “uberization” - by analogy with the famous taxi service Uber, which has significantly lowered the barrier to entry for taxi drivers. As the director of the event company Alexey Chalikov

, thanks to electronic services, classic transport companies will eventually cede the market to private owners:

The functionality of cargo transportation web services allows you to completely exclude line personnel (logistics, forwarders, managers) from the transaction, automate the process of creating accompanying documents and their transfer to the parties to the agreement. This is a clear financial advantage for private owners over owners of large fleets. But questions remain about cargo safety, insurance and compliance with delivery deadlines. If the “uberization” of freight transport is improved, this will provide a new chance for survival for private owners. As Darwin said, “It is not the strongest or the most intelligent who survive, but the one who best adapts to change.”

Uberization will not only make it cheaper, but also make the transport services market more civilized. Transportation prices can no longer be called high. For small transport owners, this service will provide direct access to orders from large cargo owners, which was previously inaccessible to them.

Alexey Chalikov , director of Heavy World.

It turns out that drivers have a choice of two options:

- join a transport company - receive transportation assignments and pre-agreed payment from it;

- become a “company” yourself - independently search for orders through electronic platforms (by the way, in theory there may also be orders from transport companies).

Both options have their drawbacks - you shouldn’t count on high tariffs from transport companies (otherwise how will they make money themselves?), and in the case of working for yourself, you will have to dump again in order to take orders from the same independent carriers.

When talking about electronic services, they often mention AutoTransInfo (which some time ago became the “ATI.SU Freight Exchange”). For example, the CEO of a logistics company Andrey Eremin

believes that ATI is the reason that the transportation market has become so transparent and low-income:

ATI is essentially a very advanced idea, especially for 1998, when the trademark was registered. They made an aggregator when it was not yet mainstream. This is surprising - many Yandex.Taxi users were not even born yet when the founders of ATI had already come up with the prototype of this service for trucks, which to this day no one can replicate. By the way, about trying to repeat it, Uber tried to launch an application about 3-4 years ago, but nothing came of it.

The most insidious thing about this platform is that it gave rise to wild competition and the concept of “return”, although before that carriers always counted round-trip rates, and if they managed to catch the cargo on the way back, it was more of a pleasant bonus rather than a forced measure. so as not to work at a disadvantage. Of course, this is an excellent way to collect statistics on market conditions, but in the right hands, these statistics turn against the carriers themselves, forcing them to work on the brink of profitability.

ATI has also become a good tool in the hands of fraudsters, since many forwarders in checking counterparties are guided only by the stars in the ATI, ignoring the simplest tricks in the form of an email address changed by one letter, for example. Not every start-up transport company can survive cargo theft and get out of the current situation with dignity in relations with the customer, and this also largely contributed to the closure of the business of many individual entrepreneurs.

Andrey Eremin , General Director.

In other words, the electronic platform simply brings customers and carriers together directly, but this turned out to be exactly what transport companies were actively making money on before. And the development of digital technologies in this case played against transport workers, bringing down tariffs to the market minimum and thereby seriously undermining their incomes

.

For the same reason, the approach to transportation has changed among customers - seeing competition for customers, they include extremely strict conditions in contracts, such as fines for every hour of delay - even if the cause of the delay has nothing to do with the driver or carrier. At the other extreme, some customers agree to cooperate only with the condition of deferred payment, which can reach up to 4-5 months.

It turns out that progress has brought the entire industry to the brink of survival. Some could not survive - in addition to hundreds and thousands of individual entrepreneurs who decided to leave transportation, one of the large ones went bankrupt a year and a half ago.

And the coronavirus pandemic has obviously only added to the industry’s problems.

What's happening in the market now

The road freight transportation market has been doing relatively well in recent years - it clearly fell during the crisis year of 2009, after which it began to grow again. Rosstat data show that the share of motor transport in cargo transportation has always been about 4-5%

– not so much due to the freight turnover of railway and pipeline transport:

But transport serves production - and if production stops for some reason, freight flows also stop. This happened all over the world in the spring of 2020 - it all started with the shutdown of many production facilities in China, and then spread to the whole world

. Already in April, the business expected serious losses, and they definitely will. Even in the base case scenario, traffic drops by 10%.

There is another approach - given that transportation directly depends on the performance of the economy (primarily production), each lost percentage of GDP gives a minus 3% to freight transportation. Considering that most departments expect Russia's GDP to fall by 5% by the end of the year, transportation could lose up to 15%.

The decline has not stopped yet - according to the same Rosstat, transportation since March has fallen below last year’s values

:

The current crisis will only aggravate the problems of the transportation market - when demand drops sharply, and supply remains at the same level (private owners cannot leave families without money, and companies cannot leave workers without wages), then transportation rates will fall further - to the limit of the minimum acceptable profitability .

However, in some places transportation has received a new impetus for growth - these are courier delivery companies in cities. Due to the previously introduced self-isolation regimes throughout the country, the demand for delivery services has increased not just significantly, but by orders of magnitude. And due to this, the segment was able to show growth, says the head of the transport company, Eduard Kholimonenko:

If we talk about small-tonnage transport, then “loners” (who have up to 2-3 units of equipment) worked as they did several years ago, and they still work now. In large cities, the demand for their services remains stable: this includes trade, moving, and intraregional movement of goods. In 2020, it even grew due to the development of e-commerce and increased demand for courier delivery. I am confident that individual entrepreneurs (as well as the self-employed) will retain their share even in the context of the further development of the large systemic transport business. Although this market is not easy for them, they need to work a lot, negotiate, look for contacts, etc., so they definitely won’t be able to sit on the stove.

Eduard Kholimonenko , General Director of Baikal-Service Yekaterinburg LLC.

On top of the existing problems, others were superimposed:

- rising fuel prices;

- devaluation of the ruble, due to which spare parts for trucks and the trucks themselves have become more expensive;

- for some time, service centers and auto repair shops could not work, and carriers could not maintain their fleet;

- increasing the recycling fee to redirect demand for cars produced within Russia, etc.

But who found it easier to survive the crisis – large companies or small firms and individual entrepreneurs?

Truck and bus markets have grown since the start of 2020

The truck (+36%) and bus (+10%) segments showed growth in January-February this year

Alexander Klimnov, photo by the author

New truck market

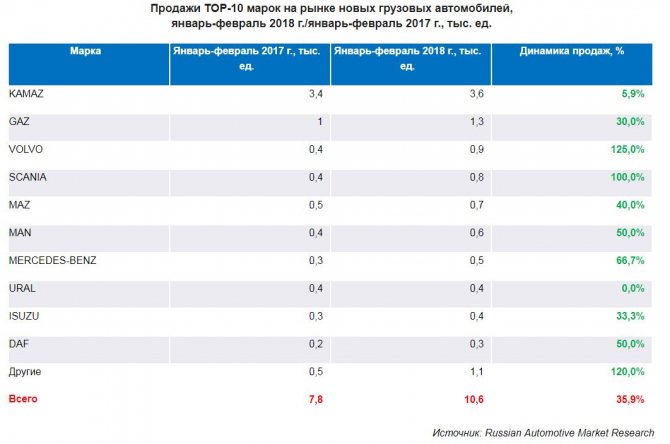

In January-February 2020, the Russian market for new trucks with a gross weight of more than 6 tons grew by 35.9% compared to the same months last year and amounted to 10.6 thousand. Directly in February of this year, 5.8 thousand trucks were sold (+35.8%).

The most popular domestic brand KAMAZ accounted for about 3.6 thousand vehicles (+5.9%), which accounted for a third of the Russian market of new trucks. Moreover, in January-February 2020, KAMAZ took an even larger share, equal to 44%.

Trucks of the GAZ brand repeated in February 2018 the same result as in the same month of 2020, occupying 12% of the market. In January-February, sales of GAZons were 30% higher than in the same period in 2020 and reached 1.3 thousand. However, its related AZ Ural showed “zero growth” with a sales volume of 0.4 thousand.

Among foreign trucks on the Russian market, the best sales figures were found among brands such as Volvo, Scania, and MAZ. Thus, registrations of Volvo trucks in the first two months of 2020 amounted to 0.9 thousand (an increase of 2.25%), Scania – 0.8 thousand (a 2-fold increase), MAZ – 0.7 thousand units. (+40%). At the same time, the third largest dynamics was shown by Mercedes-Benz with +66.7% - up to 0.5 thousand. The brands MAN (0.5 thousand) and DAF were also higher than the market with one and a half times (+50%) growth in the Top 10 (0.3 thousand). It is interesting that sales of freight brands outside the Top 10 jumped 2.2 times – to 1.1 thousand, which indicates a general revival of the market against the backdrop of a stable ruble exchange rate, when the realization of pent-up demand is pouring “golden rain” on literally every manufacturers present on the market.

New bus market

The market for new buses also experienced growth in January-February of this year, but only by 10.1%. Accordingly, registrations amounted to 1.97 thousand. However, in February 2018, sales of buses jumped by 28.3%, to 1 thousand, compared to the same month in 2020, which gives hope for more confident growth in subsequent months and good quarterly results.

More than half of the market (56.3%) of new buses is occupied by the PAZ brand. Thus, the sales volume of PAZ buses compared to January-February last year increased by 18.1% to 1.11 thousand. By the way, the related brand KAvZ showed an increase of 16.7% to 0.07 thousand. And here’s how the second one is doing the largest national manufacturer, the Likino Bus Plant (LIAZ), fared much worse after the implementation of important contracts for Moscow and the region. Thus, registrations of its medium-sized and large buses fell by 26.7% - to 0.33 thousand, which, nevertheless, made it possible to maintain second place in the market with a more than two-fold advantage over NefAZ, which became the third with its growth by 66.7% to 0.15 thousand. Only the Belarusian MAZ felt even worse in the Top 10, collapsing by 42.3% to 0.08 thousand. Even the so-called “Other” bus brands lost only 25% in total (to 0.03 thousand). It is characteristic that the places from 7th to 10th in the market were occupied by Chinese brands with an increase of 40 times (!) for Zhongtong (up to 0.04 thousand), 10 times for Higer (up to 0.03 thousand) and 4-fold for Yutong (up to 0.04 thousand) to “only” 2-fold for King Long (up to 0.02 thousand). However, Chinese manufacturers are let down by an underdeveloped dealer and service network, so sales are so far limited to one-time contracts and certain localities.

Without government support

If market participants are to be believed, small transportation companies and private drivers are living worse and worse from year to year – and this started long before the pandemic. For example, Andrei Eremin believes that in addition to the ATI system, one of its participants was involved in the destruction of the transport industry:

“Business Lines” sent a large number of small carriers to the bench due to their pricing system and strict dumping. The fact is that “Business Lines” do not make money on transportation at the time of its completion; the economic formula includes only leasing payments, office maintenance, fuel and lubricants and the driver’s salary. Earnings are included in the sale of equipment after payment of leasing payments. And individual entrepreneurs, without realizing it, support an economic scheme that is killing them, buying Business Lines trucks just below the market, not realizing the fact that Business Lines has already taken this difference from him tenfold at the expense of the profits that he didn't receive enough Such is the irony of fate.

Andrey Eremin , General Director.

In addition, the expert believes, transport workers are not very popular in banks and the tax service. Thus, the Federal Tax Service considers this market risky from the point of view of cashing out money, and because of this, banks set higher commission rates for companies with the corresponding OKVED codes.

And there is also a problem with VAT

. The fact is that it is more profitable for shippers to engage carriers who work with VAT - this way they receive the right to a tax deduction (this is the essence of VAT itself), and the tax office does not have unnecessary questions. According to Andrey Eremin, because of this, intermediaries in the form of freight forwarders appeared on the market. They officially work with VAT, but in fact private traders work for them - without VAT. And these private owners also lose because they cannot return VAT on purchased fuel or spare parts, since they themselves are not included in the supply chain.

also told us about the role of the tax service in industry transformations :

For many private entrepreneurs and individual entrepreneurs, 2020 becomes a turning point in deciding whether to continue working in this market. Firstly, at the moment there is a strong imbalance in the supply of road transport services due to a shrinking market due to the coronavirus. Secondly, VAT calculation schemes without VAT have practically disappeared, or the cost of this scheme has increased by 2-3 times due to active actions on the part of the Federal Tax Service. Because of this, small carriers cannot enter into contracts with customers since the latter are on the general taxation system, and the vast majority of individual entrepreneurs are on UTII. Thirdly, the indirect “Plato” tax appeared.

Given this state of affairs, private carriers operating in narrow niches, those who have business connections with large customers, and self-employed people who do not pay payroll taxes may remain on the market. Those who work through forwarders and/or through the ATI.su exchange will leave the market.

In 2021, with the introduction of the electronic consignment note and the abolition of UTII, most small carriers will stop operating or switch to working as part of the transport departments of federal companies.

Oleg Vasiliev , deputy director of ANO DPO "SZRTsOT".

will not receive serious support from the state in 2020

, even if they work absolutely legally. All types of assistance (interest-free loans, salary subsidies, tax exemptions for the second quarter) were received by business from among the most affected industries - but among the carriers there is only air transport.

Only the self-employed

(professional income tax payers), but taking into account the peculiarities of calculating NAP, there are few self-employed among transport workers.

Assembly under license using the example of tractors and bulldozers: gaining momentum

When it comes to crawler tractors and bulldozers, there are many small manufacturers that are too many to count and not visible on the market due to their small size and lack of significant advertising. These are manufacturers-assemblers who operate under the license of ChTZ and Promtractor. Moreover, licensed assemblers of ChTZ cars are geographically, which is understandable, grouped in the Chelyabinsk region, but at the same time in Chelyabinsk itself they also sell licensed Chetra.

Licensed manufacturers of tractors and bulldozers "ChTZ" still buy diesel from the original manufacturer, and are forced to buy both the frame and tracked bogies there. Drive wheels, tension wheels, and road wheels are taken from ChTZ, Promtractor, and Ural crane repair plants.

Licensed assembly for the modern Russian market of special equipment is very interesting and profitable. 2-3 large factories throughout Russia will still not have time to “serve” all interested customers, especially since the products of licensed assemblers are 1.5-2 million cheaper (at a minimum, they do not need to maintain as many staff as at, and pay such taxes).

Of course, there are also low-quality “licensors” who take the same road wheels from underground production, violating their manufacturing technology, which only large enterprises with experience can do. They can take a used diesel engine and pass it off as a new one, or a “rebuilt” old car as a newly assembled one.

This is why customers need experienced suppliers like: we can weed out bad licensed assemblers and work with conscientious ones . Of course, the customer should not contact unknown companies directly to purchase a B10M bulldozer. Otherwise, high-quality “licensors” who offer B10M for 4.5 million rubles, which from the original manufacturer would cost 5.5-6 million without taking into account the “salvage fee”, are extremely useful for the market, and their products sell well here. They assemble from several cars a year to a couple of dozen; in terms of quality, they can achieve the famous “European” manual assembly if they take high-quality components. They don’t use complex things like hydromechanical transmission, but they offer a machine at an affordable price with the necessary universal set of equipment - a straight or hemispherical blade, a pick, a towbar.

About the used special equipment market: how scary it is to throw away the old

It is impossible not to mention the market for used special vehicles in 2020. On the one hand, we recently had a period (approximately 2015-2016) when for the most part only spare parts, “overhauled” and “licensed” cars were sold. At that time, we quickly tried to change our strategy and pay great attention to machine repair - we offered both refurbished bulldozers and motor graders, and repaired diesel engines and control units for truck cranes. In 2020, when there was a clear focus of the state on large projects in the field of construction and the military-industrial complex (for example, the construction of the Kerch Bridge), sports infrastructure, and the construction of gas and oil pipelines continued to develop, we recorded an increase in demand for new cars. At the same time, the licensed assembly was also sold well.

However, one should not hush up the truth that only very large customers have the money for this. Small and medium-sized construction companies that fight for irregular orders often cannot afford a new original ChTZ or Chetra bulldozer, much less a drilling rig based on it. If, for example, a new Ivanovets truck crane with a lifting capacity of 25 tons can be purchased for no less than 6 million rubles excluding salvage fees, then the same machine produced in 1995-1996 can be found on the avito.ru portal for 400-500 thousand rubles. This is a “wild” market, it does not guarantee anything, and the condition of the car may be sad. However, the construction order may not be large, and the probability of winning it from a certain company is not 100%.

The recycling fee in our market, which threatens to increase further in 2018, is pushing many customers to look for refurbished used cars, preferably at a cheaper price. In addition, there is also a clear tendency that can be compared with the accumulation of old things in almost every Russian apartment: storing old things is inconvenient, unpleasant to wear, but you also don’t raise your hand to throw away old jackets and coats, knowing that there will be no money for new ones. I remember how the older generation knew how to repair, restore, and used the “do it yourself” principle. When people have little money, the principle of restoring the old and maintaining its performance “until the last” is universal - from the apartment where an ordinary Russian family lives, to an old motor grader that periodically receives orders in its town.

Our advice:

The only thing that can be advised to such customers, and there are a lot of them (as they say, “don’t teach me how to live, better help me financially”) is not to buy special equipment “second-hand” on bulletin boards on the Internet. It’s better to contact professional suppliers, including us - we will select decent used equipment, help with repairs, and monitor the quality. If in some Russian city an old RDK-25 crawler crane has been on sale for a long time, we know about it and will be able to tell you what is “firewood” and what needs to be restored, and we will do it ourselves, we will even be able to give some kind of guarantee.